by John Glier

Editor’s note: This article was updated on May 29

We’ve never experienced anything like the current COVID-19 pandemic.

The current public health crisis has upended everyone’s lives. We’re still not beyond the peak of the crisis and the World Health Organization reports that there have now been more than 5.7 million confirmed cases of the disease worldwide and nearly 358,000 deaths across 216 countries, areas and regions around the world. There have been nearly four times more cases, and more than twice as many deaths, in the United States as any other country. Given the lack of widespread testing in the United States, it’s likely that countless more have been afflicted by this virus. With the 12- to 18-month estimate for an effective vaccine, those numbers will continue to grow.

This health crisis has indeed precipitated volatility in the capital markets, and widespread unemployment across the globe. Already, more than 40 million U.S. workers have filed for unemployment benefits in the last three months. The U.S. unemployment rate reached 14.7% in April and Federal Reserve Chair Jerome Powell recently acknowledged that it could climb as high as 25%. The virus has stalled the U.S. economy and foretells a steep drop in gross domestic product in the second quarter of this year.

The International Monetary Fund’s (IMF) mid-April projections described the coronavirus pandemic as a “crisis like no other,” with considerable uncertainty about what the economic landscape will look like when we emerge from this lockdown. The IMF predicted a global economic decline of 3% this year, which would be the worst recession since the Great Depression. However, assuming the pandemic fades in the second half of 2020, and public policy initiatives successfully mitigate the virus’s impact, the IMF predicts a rebound in growth of 5% in 2021.

Many, but not all, nonprofits have seen declines in giving over the past 10 weeks. To be clear, we have also seen a remarkable response to the urgent needs precipitated by this crisis in health care delivery, for COVID-19-related research, and to address the many impacts this pandemic has had on students and colleagues, our families, our communities, and our daily lives. Many donors, wherever they have been deeply engaged, have continued to support a range of program initiatives. So, what does this likely recession we’re facing mean for philanthropic giving?

While we don’t have a crystal ball, and most would agree that this is an unprecedented health and economic crisis, we might look to the four business recessions in this country over the past 40 years to provide us with a few clues.

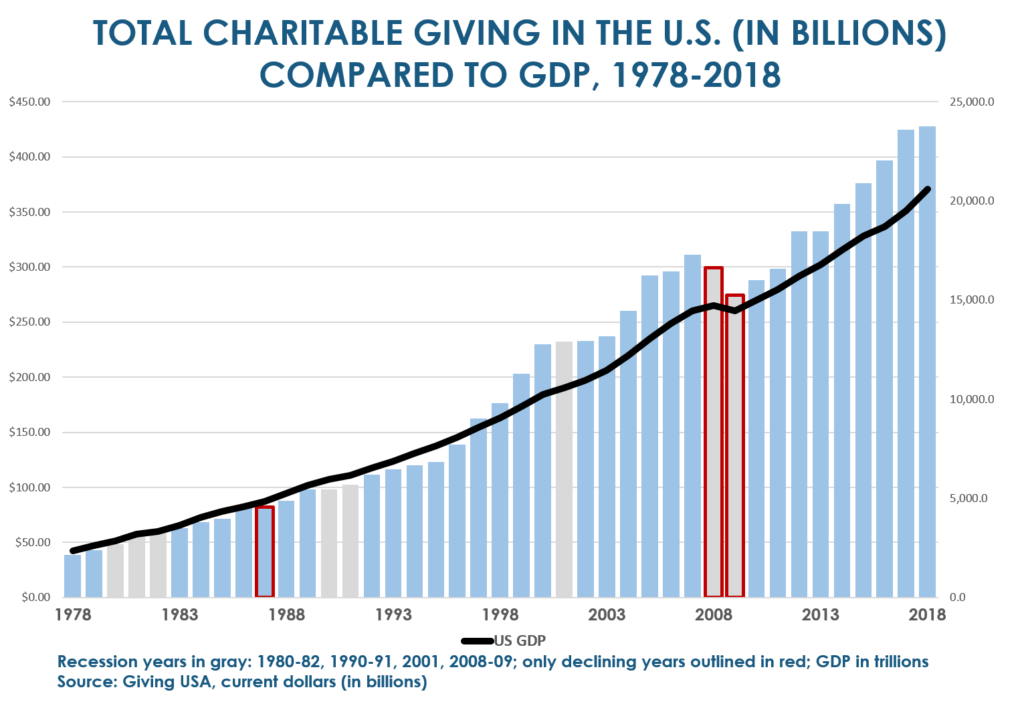

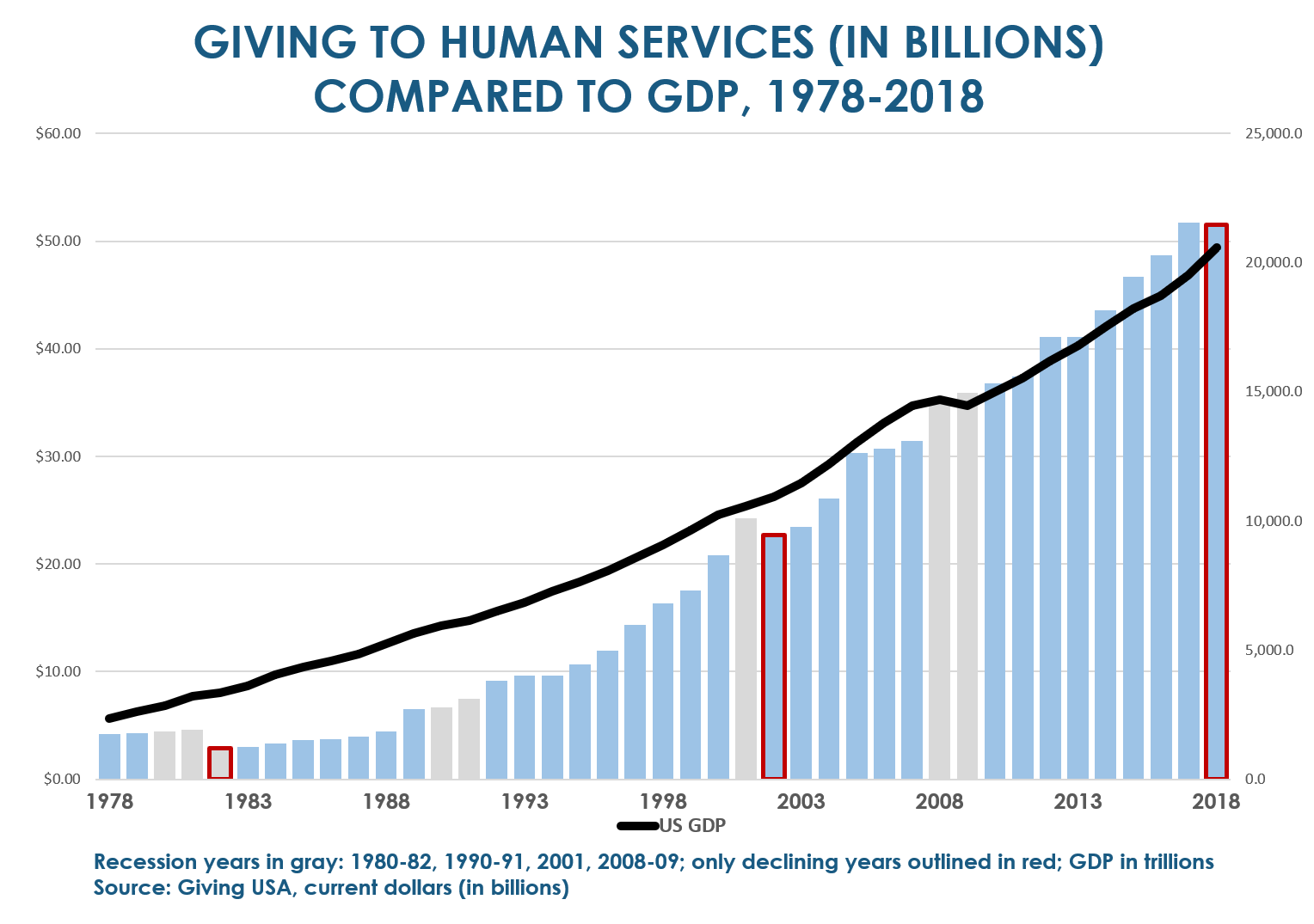

Philanthropic giving over the past 40 years

Here’s a look at total charitable giving over the past 40 years and the four recessions experienced by the U.S. economy. Total giving has closely tracked the steady rise in U.S. GDP, and cash from all sources has remained roughly constant, at 2% of GDP throughout this period:

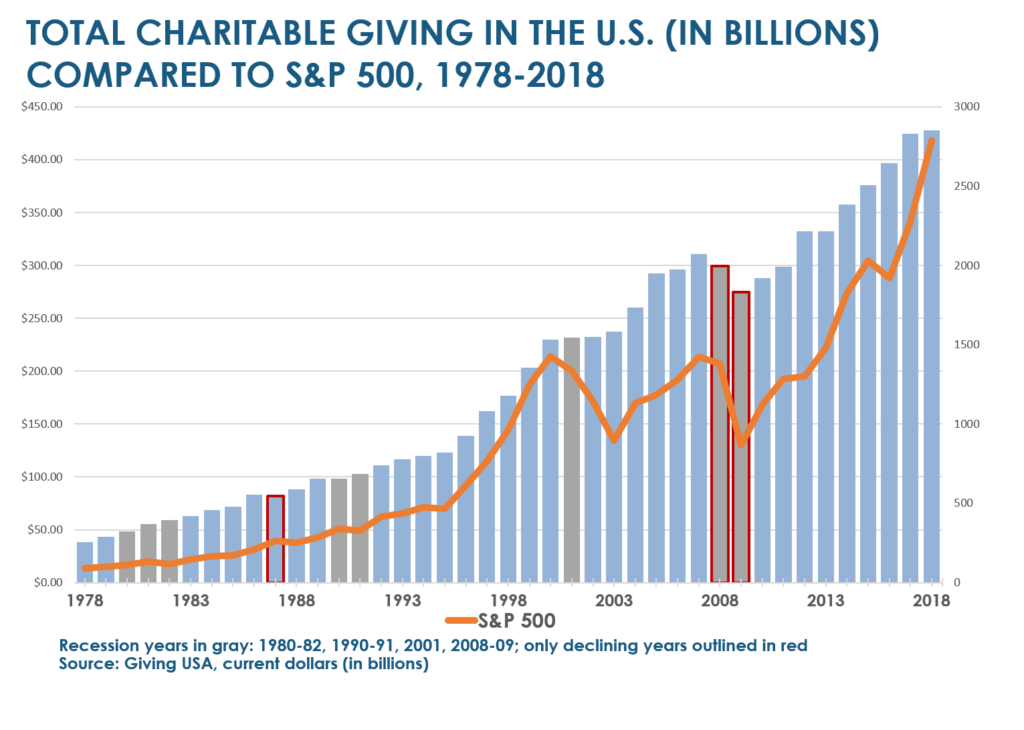

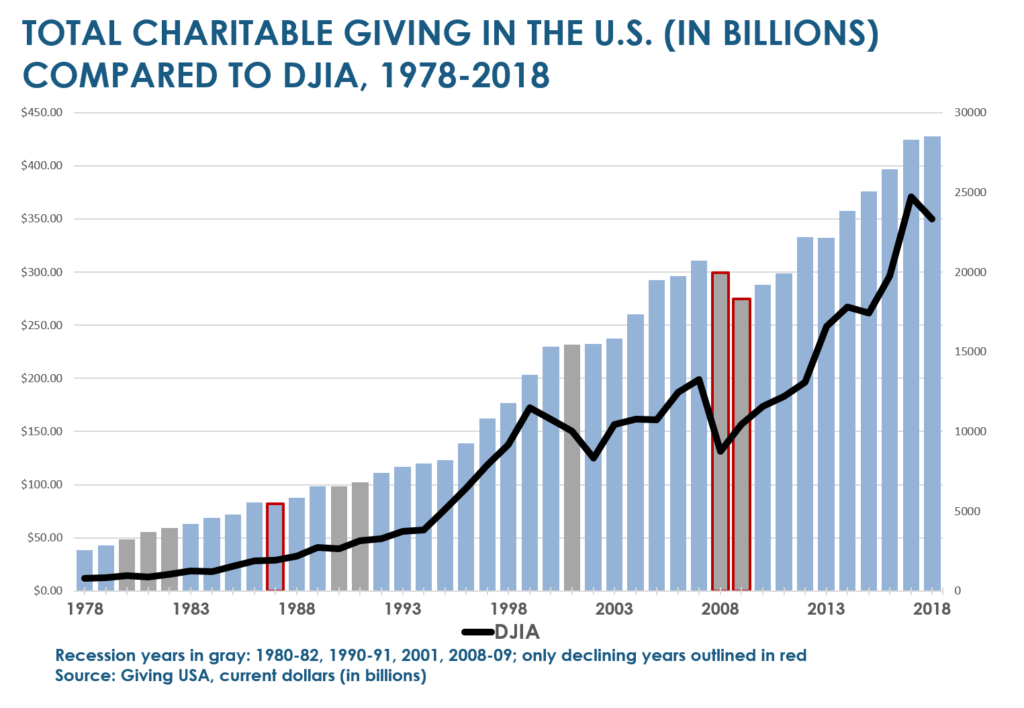

The two charts below provide a picture of two market indices, S&P 500 index and the Dow Jones Industrial Average, and how they align with charitable giving activity.

What is remarkable in these charts is the extraordinary resilience of giving across the United States.

During the 1980-82, 1990-91 and 2001 recessions, total giving actually increased in each of those six years, despite declines in U.S. GDP. Immediately following those recessions, total giving moved to a succession of new highs.

While the “bounce back” was slower following the 2008-09 recession, total giving hit a new high within three years.

Of course, in many ways the remarkably fast and dramatic decline that we are currently experiencing is markedly distinct from other recessions. It is both a public health and economic crisis, with a troublesome outlook for Main Street.

“Numbers coming out of the second quarter will not be comparable to anything we’ve seen in U.S. macroeconomic history,” said James Bullard, president and CEO of the Federal Reserve Bank of St. Louis in a mid-April webinar. In March, he suggested that the unemployment rate could soar to more than 30% and U.S. GDP could decline dramatically in the second quarter.

However, Bullard believes the economic crisis can end with a V-shaped recovery—if there is a high level of testing by the third quarter that enables healthy people to return to work.

Similarly, Goldman Sachs’ economists expect U.S. GDP to decline 34% in the second quarter from the previous quarter on an annualized basis, with a quick recovery that includes 19% and 12% growth in the third and fourth quarters, respectively. But they also note that their forecast is heavily dependent on the United States implementing a carefully considered reopening strategy that hinges on a sharp ramp-up in testing and contact tracing.

We might add that both Bullard and Goldman Sachs Chief Economist Jan Hatzius believe the hangover from the crisis is unlikely to last as long as the recovery from the 2008-09 recession given the absence of any major economic or financial imbalances heading into it.

Giving rebound amid rising capital markets

If that proves true, we believe it would be very good news indeed for our nonprofit institutions. While the current market volatility, asset losses, and the widespread impact of the pandemic will certainly slow the immediate pipeline for major gifts—at least for the short term—we believe it is likely we will see giving rebound as we begin to see stronger economic forecasts, and rising capital markets.

To be sure, we are hearing across our client base in North America remarkable stories about how giving has persisted as this crisis has unfolded—at every level. Some have reported “record-level” Giving Day participation and cash; others have cited the closure of any number of large-scale gift discussions—some indeed to support COVID-19-related initiatives, and others still very much focused on their institutional core mission.

It is also worth noting that the context for our current predicament is the Tax Cuts and Jobs Act of 2017, which contributed to a 1% decline in individual giving in 2018 (3% in inflation-adjusted numbers). The tax cuts and, in particular, the change in itemization rules, have clearly contributed to 2018 being the first time that individual giving comprised less than 70% of overall giving in the last 50 years. On an inflation-adjusted basis: we saw arts, culture and humanities giving decline 2% in 2018; health giving decline 2%; education giving decline 4%; and giving to religious causes decline 4%. Other recent studies of giving in the United States underscore a broader decline in charitable giving across the country since 2000. We have seen a 13% decline in U.S. household giving, representing more than 22 million fewer donor households since 2011, along with a decline in volunteer activity across the United States at almost every level. Meanwhile, high net worth households—though fewer of them—are contributing larger and larger gifts, driving total giving in 2018 to a record $427.71 billion.

Our long experience in the sector suggests that many donors will likely continue to give during such recessionary periods, especially if asked. Their giving patterns appear to change, with their focus upon fewer organizations—the institutions where they’ve been most engaged and committed in the past. We’ve also observed that well-established nonprofits with a diverse constituency of donors—and especially those engaged in proactive fundraising campaigns—will fare better than others, especially if they sustain their campaigns, and continue their solicitation activity.

As we look closely at different segments of the nonprofit community, there are some notable differences in the ways donors have responded in times of economic stress and downturn.

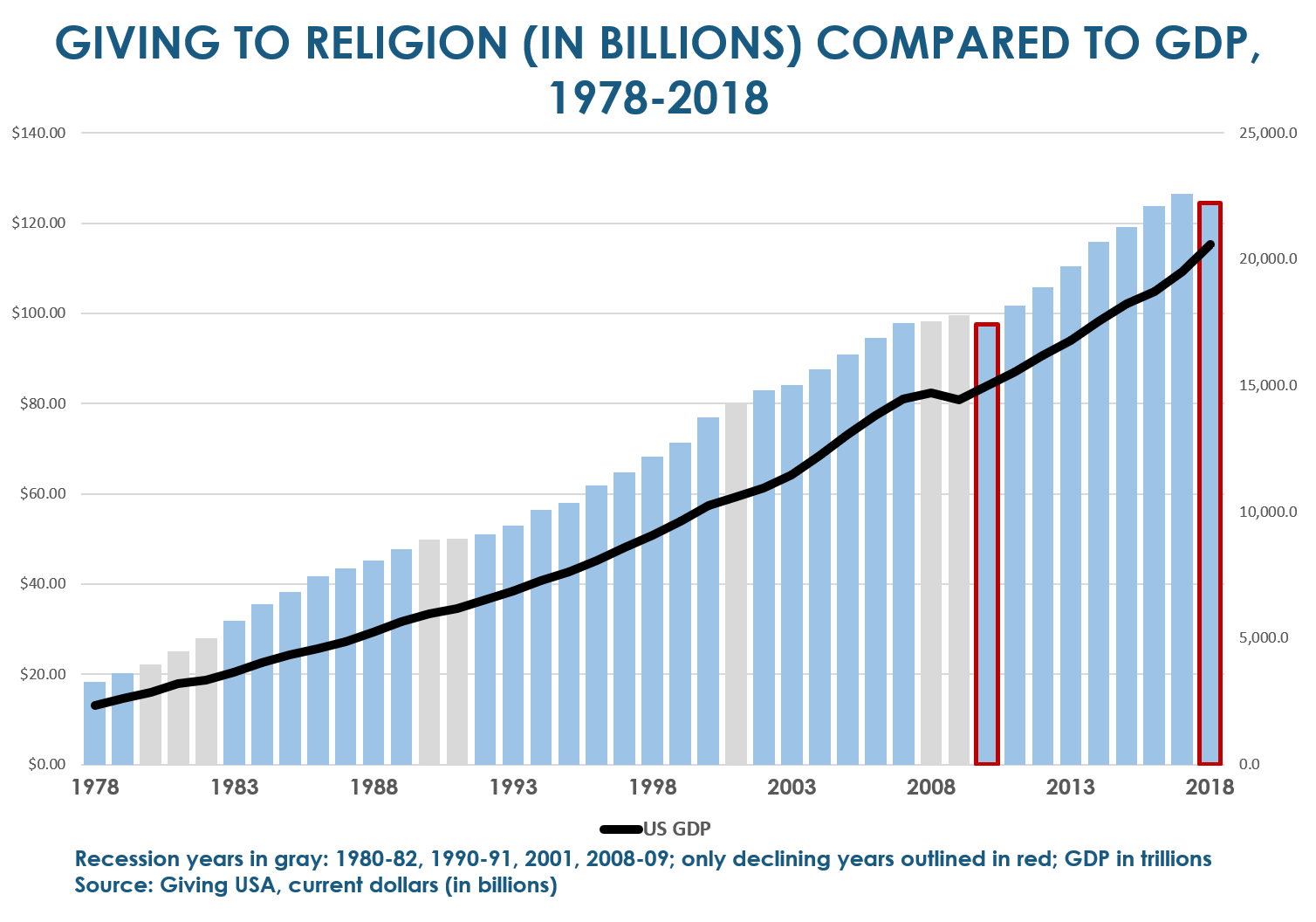

Giving to religious organizations tends to be somewhat more resilient during recessions, although its share of overall giving in the United States has declined from 47.6% of total giving in 1979 to 29.1% in 2018, a 39% decline over 40 years.

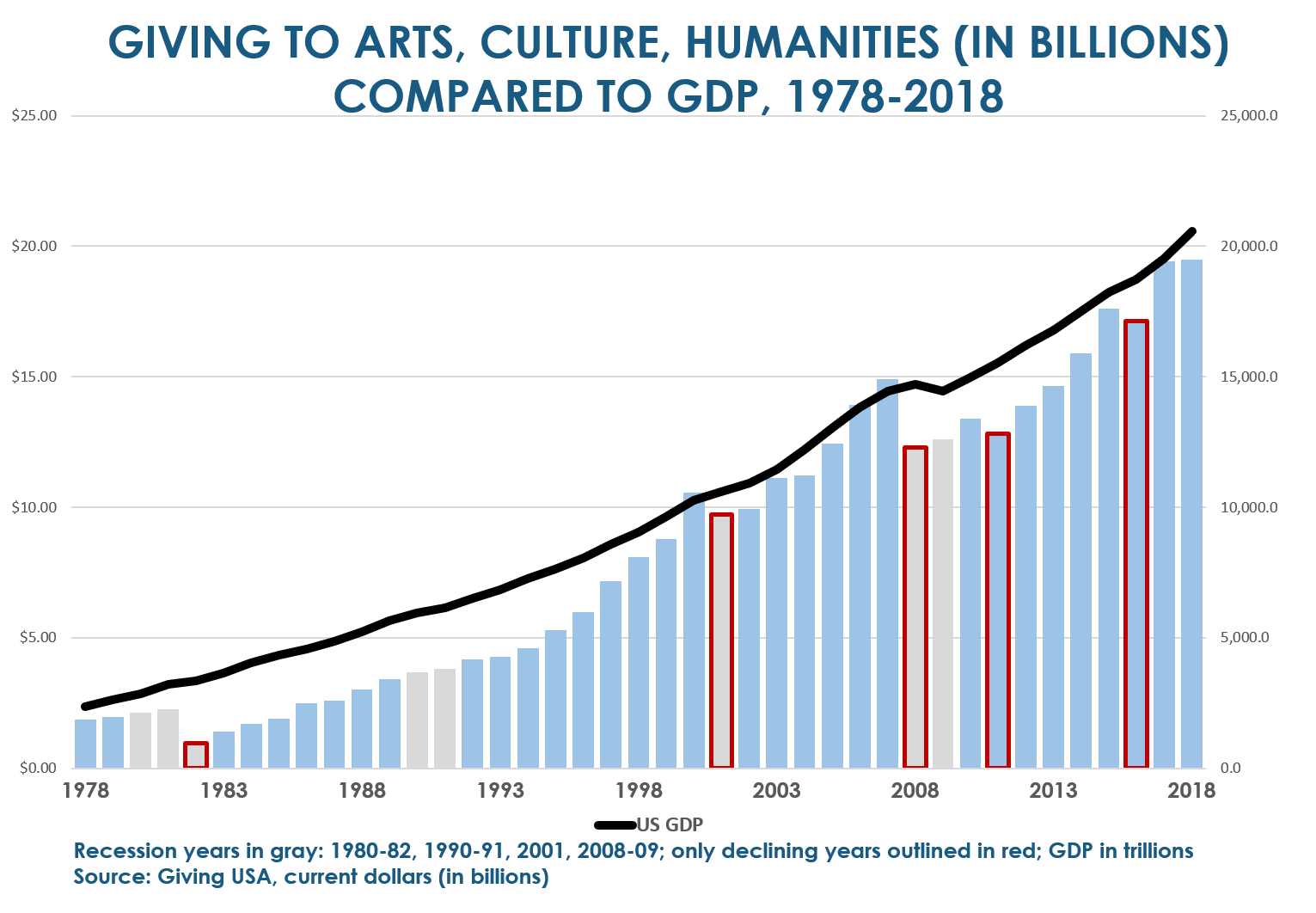

Among arts, culture and humanities organizations, giving has been somewhat less resilient. For example, it was not until 2014—seven years after its 2007 peak—that giving in this area recovered from its 18% decline in 2008. Similarly, after a 58% decline in 1982, giving began to recover with a 45% jump in 1983. But it did not fully recover to its previous high until 1986.

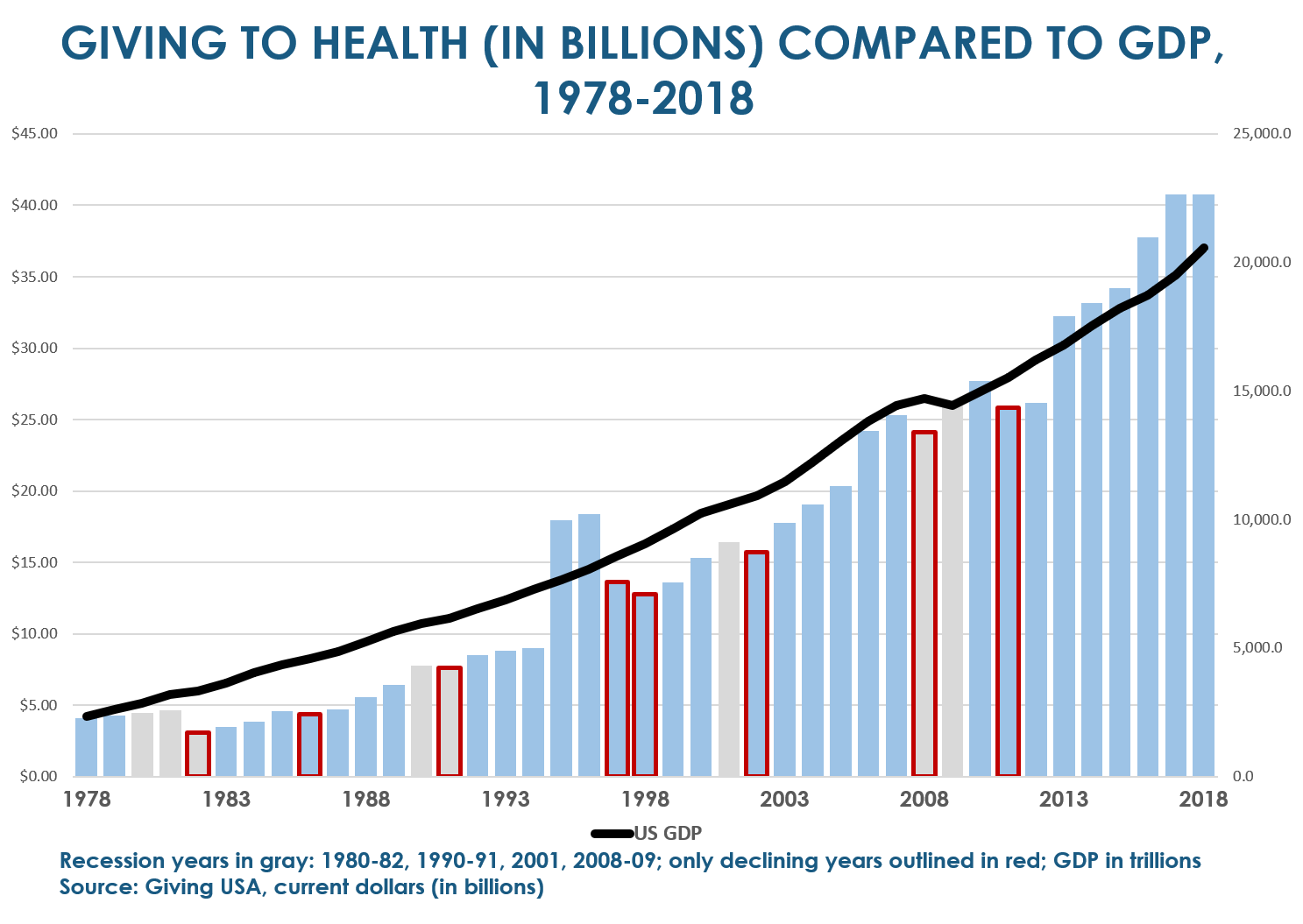

Giving to health care has been more chaotic than other sectors in the wake of economic slowdowns; giving fell roughly 5% in 2008, 2% in 1991 and nearly 34% in 1982. Even so, giving in this sector rose immediately following each recession over the past 40 years, except in 2002, when it took a year to bounce back.

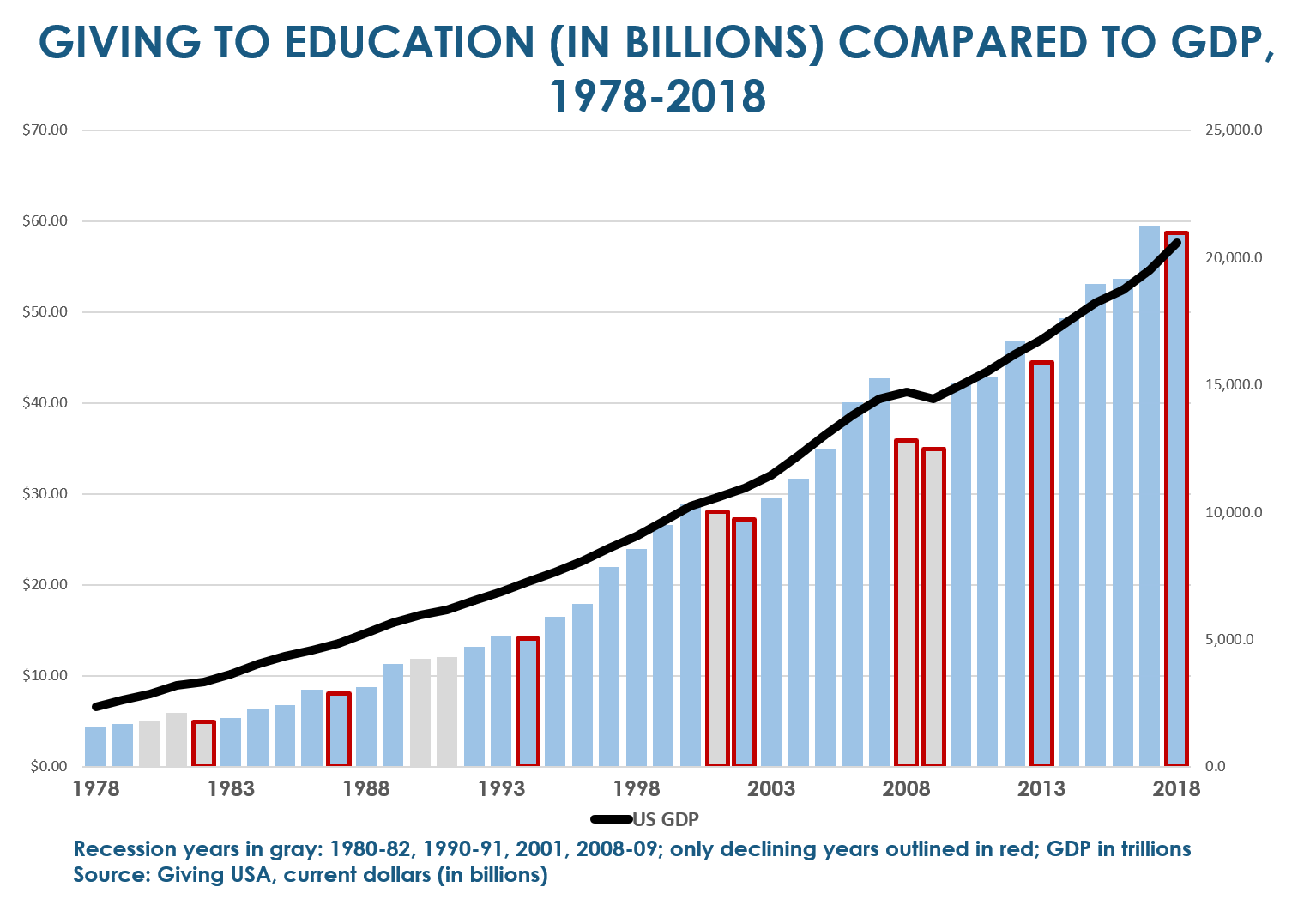

For educational institutions, the Great Recession was particularly difficult both in 2008 and 2009, when giving fell first 16% and then 3% in those two years.

That said, giving to education hit new highs within a few years after each recession. We should note that the slowest return to a new high was following the Great Recession when it was 2011—four years after the previous peak in 2007— before giving to education had fully rebounded.

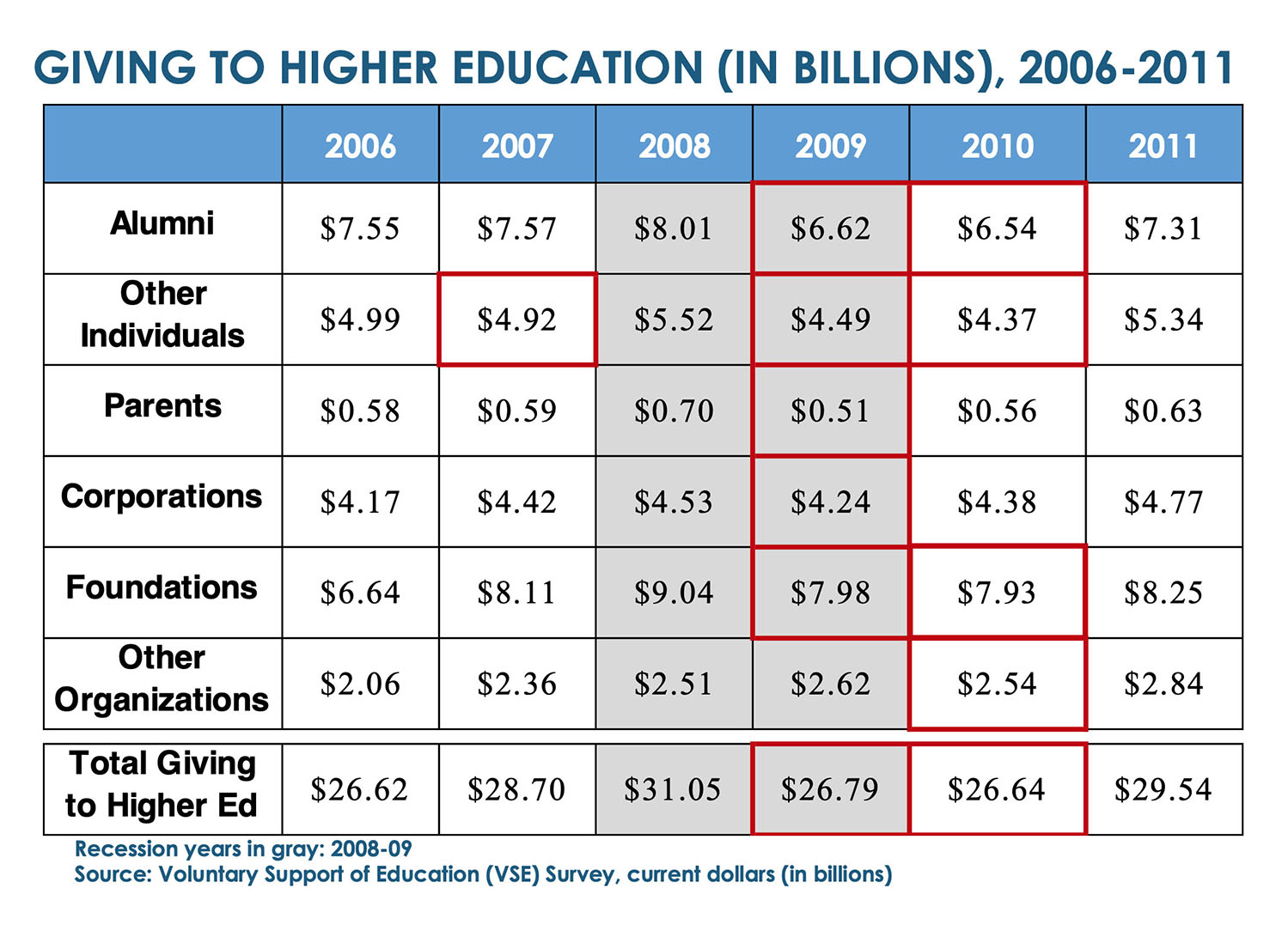

For a closer look at giving to institutions of higher education, we reviewed the Voluntary Support of Education (VSE) Survey results from 1978 to 2018. All six VSE sources of giving to institutions of higher education—alumni, corporations, foundations, parents, other individuals and other organizations—had only modest declines in giving in 2001 and, by 2002 giving was up significantly across the board in each VSE category. There was also only minimal impact following the 1990-91 and 1980-82 recessions. We saw a much steeper decline during the Great Recession when overall giving to higher education fell 14%, driven by a 27% decline in parent giving, and a 17% decline in gifts from alumni.

What perhaps is one of the more encouraging statistics, and a reminder of to what degree individual giving drives these numbers, Americans during the Great Recession stepped forward and increased their giving to Human Services in 2008 by 12.4% ($31.5 billion to $35.4 billion) and again in 2009 by another 1.4%.

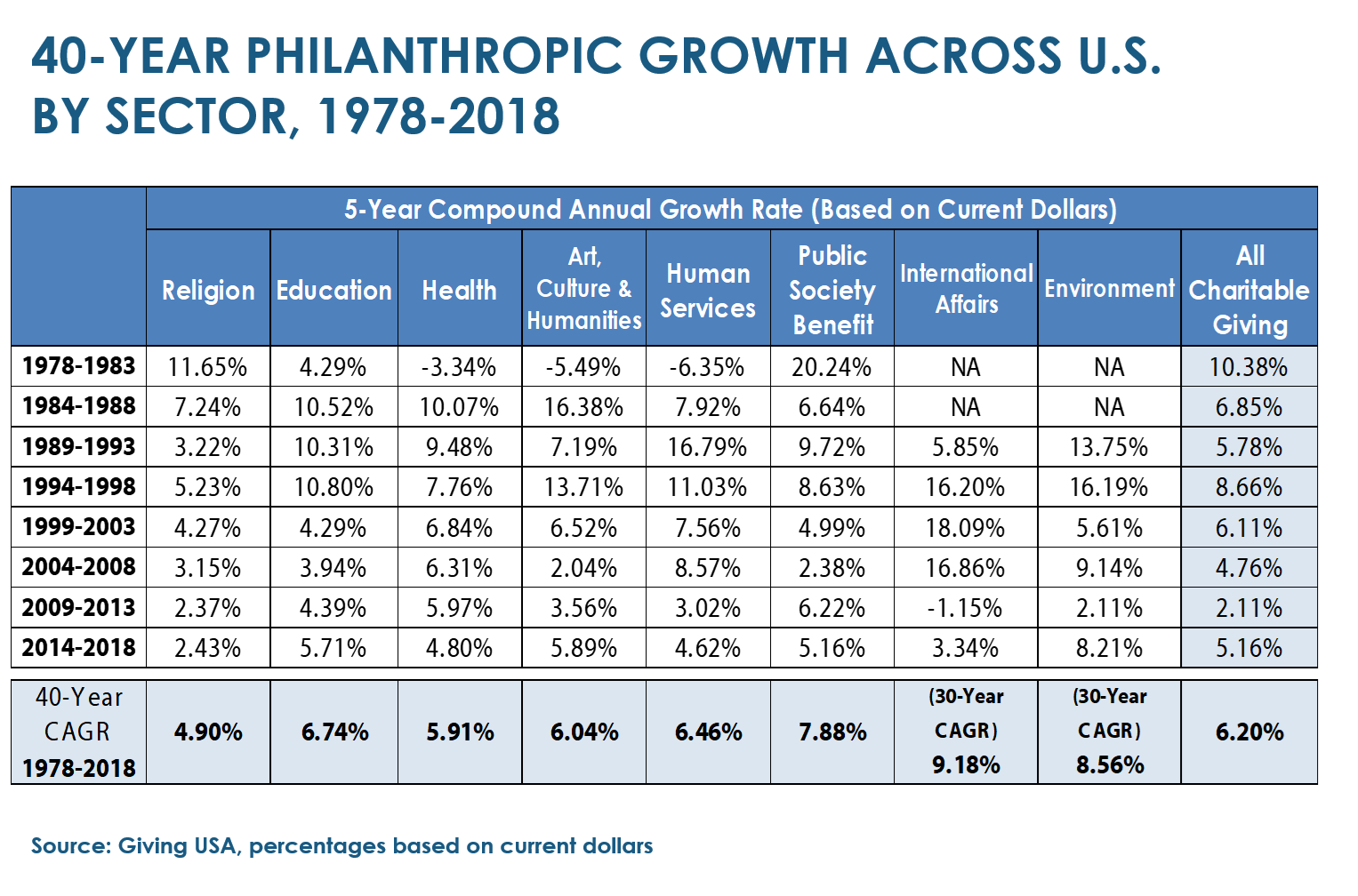

Finally, while we’ve come to expect years of pronounced contraction in philanthropic activity during years of recession, we’ve also witnessed the remarkably steady 40-year growth in giving across all these sectors, framed below in five-year compound annual growth segments. Such reliable growth has kept pace with the growth in U.S. GDP, as well as growth in the S&P 500 index and Dow Jones Industrial Average.

Looking ahead

So, how will philanthropic giving react to our current crisis?

Some of this data suggests that rising equity markets will often inspire philanthropic growth rates much more reliably than declining markets will slow them down. Perhaps it’s fair to say that bear markets are not to be feared so much as bull markets are to be cheered, when it comes to our philanthropic growth aspirations. It is, after all, the appreciated assets in those markets that often fund the larger gifts and the steady growth we’ve seen in U.S. philanthropy.

As we look at how the United States—and other countries around the world—are dealing with this unparalleled health and economic crisis, we are all searching for a basis for cautious optimism. The dramatic steps that government policymakers around the world have taken to “flatten” the curve have slowed the pace of this pandemic. No one, however, can predict what might happen with a resurgence of the virus in the fall, where indeed the capital markets might be, or how much damage we are likely to see on Main Street in the aftermath of so much employment and business failures.

Moreover, the crisis has driven people together in ways that were unimagined just a few months ago. People are sewing masks for friends and family, donating meals to health-care workers and offering help to neighbors in need. Many have doubled down in support of cherished nonprofits and have expanded their giving to COVID-19 relief and research initiatives. Our leadership institutions quickly pivoted to undertake a remarkable range of virtual engagement initiatives, sustaining long-term relationships, and beginning new ones.

What the “post-pandemic” world looks like for philanthropy is difficult to predict, but we will likely never be the same. Given what we have seen with respect to giving and past recessions, we do expect to see extraordinary giving return in the coming years, or perhaps even months, and a robust surge to even higher philanthropic levels. Donors will most likely feel a renewed sense of purpose around their giving, especially in the wake of all that we have experienced. Our nonprofits, those that have seized upon this crisis as an “opportunity not to be lost,” will have learned new skills, deepened and perhaps broadened their communities of support, and built a post-pandemic plan for even more substantial philanthropic growth in the years ahead. This pandemic is likely to have led us to a new “normal” that few of us would have ever predicted.

John‘s counsel is available to your organization as part of GG+A’s new Virtual Resources for Advancement Professionals offering, which you can read more about here.