Are You Overlooking Your Mid-Level Donors? Here’s How to Prioritize...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Five Crisis Communications Best Practices for Higher Education Leaders to...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

New Year, Same Annual Fund: How to Develop Fresh Messages...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

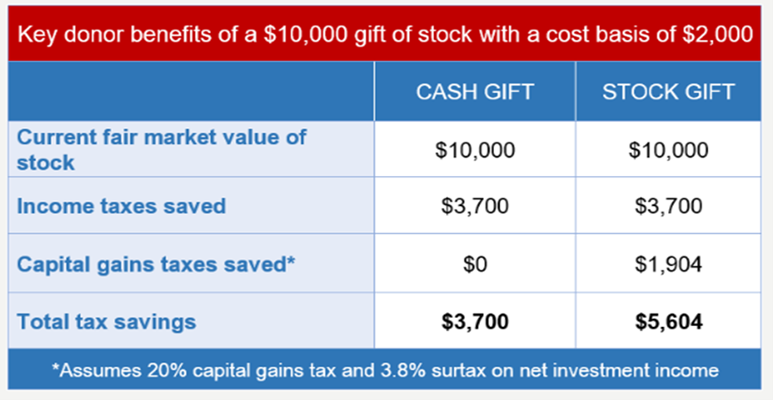

Smart Year-End Giving Options to Explore with Your Donors While...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Leveraging AI for Donor Pipeline Development: Practical Strategies for Fundraising...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Build a Robust Corporate Giving Program for Impact and Sustainability...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Establishing Effective Major Gift Metrics for Your Independent School In...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The Call for Donor Engagement: Why It’s Time to Rethink...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

How to Build a Planned Giving Culture – and Why...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Keys to Developing a High-Value Fundraising Programme: Insights for Global...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Prioritize These Capabilities in Principal Gifts Fundraising For those institutions...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Three Essentials for a High-Performing Principal Gifts Team As wealthy...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Prospect Development: Rethink How You Categorize Prospects Prospect development teams...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Increasing Alumni Participation in Annual Giving is Still a Great...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Three Key Takeaways for Arts and Cultural Institutions from the...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Develop a Major Gifts Program That Attracts Ongoing Investment I...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

CRM Systems and Change Management: 3 Principles to Help Your...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Donor Qualification: How to Get the Meeting and Attract Future...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Benchmarking in Healthcare: The Data You Need to Protect Resources...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

How to Fundraise without a Fundraising Staff Attracting and retaining...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Four Essentials for Strengthening Relationships with Your Board and Volunteers...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Is it Time to Make a Change? Four Steps Every...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Strengthening Fundraising Partnerships in the C-Suite: Keys for Development Officers...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Fundraising for Social Justice: 5 Keys to Success for Museums...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Strengthen Your Campaign Planning: Leveraging Provosts as Key Advancement Partners ...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The AI Revolution and Its Implications for Advancement Teams With...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

How UK Charities Can Demonstrate ROI in Their Fundraising Programmes ...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Analytics: The Data You Need to Strengthen Your Advancement Program ...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

High-Impact Donor Stewardship: Value Your Donors and Advance Your Fundraising...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

3 Keys to Guide Your 2023 Communications Strategy It’s the...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Combat “Donor Fatigue” with These Tips to Revitalize Your Fundraising...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

How to Make Your Annual Fund Appeals More Appealing (and...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Maximize Year-End Giving in an Unpredictable Economy Regardless of how...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Our Top 5 Thought Leadership Articles of 2022 As a...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Principal gifts are more than just bigger major gifts. They...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Refocus Your Independent School Advancement Team on Metrics That Matter ...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

As with many nonprofit organizations, independent schools rely on a...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Gifts of appreciation for a donor or member’s generosity can...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

As women’s share of national wealth grows and their impact...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

GG+A Note: This post was originally published in May 2020...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Despite ongoing gains with improving diversity, equity, and inclusion in...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Earlier this year, I had the opportunity to speak with...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Fundraising institutions such as academic medical centers have become increasingly...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

At Grenzebach Glier and Associates, we believe that fostering an...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

How Advancement Professionals Can Leverage a Methodological Approach to Affecting...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The question of whether annual giving days have exhausted their...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

As fundraisers, we hear with some frequency from trustees and...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

We often see development office activity slow down after the...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Donors’ gifts to your organization are signs that they have...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Events have long been an important component within our fundraising...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

It’s been easy for institutions to get swept up in...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Here are three lessons we learned last month: Mentorship conversations with...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Issues matter more than ever. That’s the takeaway from a...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Managing a development program is fraught with challenges. Add on...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

We’re in the midst of a moment of dramatic change...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Here are four lessons we learned last month: Our...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This Thursday will mark the conclusion of the CASE Summit...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The pandemic has had a profound impact on many people’s...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Here are four lessons we learned last month: 12% of annual...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Essentials of a Well-Planned Annual Fund: Hope Is Not a...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

It's hard to overstate the importance of end-of-year giving. Nearly...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

You don’t need to be the most colorful writer to...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Here are four lessons we learned last month: Now is a critical...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Most major gifts don’t just happen. They stem from years...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Whether an institution has a reliable base of volunteers that...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The COVID-19 pandemic drove an influx of new donors to...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Here are four lessons we learned last month: The Olympics provide a...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

High employee turnover is a serious problem that has serious...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Feasibility study results are dependent on the donors who are...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The COVID-19 pandemic presented a shocking stress test to nonprofit...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

There’s a lot more to annual giving than meets the...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Volunteers want to help. They want to contribute to your...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Here are five lessons we learned last month: Overall giving...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Ensuring that donors are satisfied with their giving experience is...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The COVID-19 pandemic fundamentally altered the way that many of...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Overall giving reached $471.44 billion in 2020, setting a new...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

(Editor’s note: This article originally appeared in the Chronicle of Philanthropy)...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Do you have ambitious campaign aspirations but not much experience...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Grenzebach Glier and Associates believes that fostering a diversity of...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Here are four lessons we learned last month: Behind every...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

What inspires parents to volunteer? Keeps them engaged? Makes them...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Academic medicine and healthcare institutions have unique opportunities to leverage...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Many of us have been remotely engaging our boards for...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Here are four lessons we learned last month: It is...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Volunteers are the lifeblood of nonprofit institutions. They are often...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Note: This article originally appeared in the Spring 2021 issue...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

We’re in the midst of a significant moment for planned...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

If all goes according to plan, the United States will...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Here are four takeaways we learned last month: A good...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Campaigns are longer than ever. The median capital campaign spans...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Too often independent schools take a “tent-like” approach to major...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In a little more than a decade, GoFundMe has grown...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Whether in a campaign or not, the board of trustees...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Here are five lessons we learned last month: Comprehensive fundraising...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Over the course of 25 years in fundraising, I’ve collected...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Anyone who works in higher education knows that leadership changes...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Your board of trustees has just approved a proposed capital...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Boards can serve an extremely important role within a nonprofit...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

A number of university advancement leaders have recently asked me...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Andy Shaindlin, Vice President for Alumni Relations, recently spoke with...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In the course of a few days in March, the...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Here are four lessons we learned in January: Advancement officers...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

When most people look back on their university days, they...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Treasure Valley Family YMCA CEO David Duro was floored when...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

During my 35-plus years in development I’ve held fast to...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Let’s imagine a common scenario. Soon you’ll be sending an...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Montgomery College, a three-campus community college, in December 2019 received...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Raising money in the midst of a global pandemic and...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Only eight months into the leadership gifts phase of its...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In the webinar “Virtually Interactive Homecoming From Home” Kutztown University...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Even in normal times, institutions are likely to know far...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Along with other facets of Advancement, the pandemic has deeply...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

It’s November: time for most annual giving directors to be...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

We live in the age of personalization. Whether donors are...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

GG+A President Suzanne Hilser-Wiles recently appeared on “The Development Debrief”...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

It’s easy to count inputs. That’s why nonprofits have long...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

With the world changing at a rapid pace, there has...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

October’s outlook on fundraising has remained somewhat steady with September...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

There is growing recognition inside academia that solutions to both...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Whether you are an advocate or a skeptic of strategic...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Looking out 90 days, just eight (8%) of respondents see...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Senior Director of Annual Giving Nicole Brennan, CFRE and Program...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The global pandemic, recession, and racial reckoning have challenged nonprofits—particularly...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Nonprofit institutions have never experienced anything like the last six...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

It is difficult to escape the reality that these are...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

What would you think if I told you in December...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Alongside “COVID-19” and “pandemic," it is reasonable to assume that...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

September responses show a slight downturn in the 30, 60,...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The fall term is upon us and COVID-19 still looms....

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This is the third article in a three-part thought leadership...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Congratulations. You made it through FY20. Perhaps your school’s fundraising...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Loyola University Maryland’s Terrence Sawyer, J.D., Senior Vice President Advancement,...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In this week’s survey of fundraiser outlook, we learn that...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This fall will look dramatically different from any previous year....

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Jim McKey, GG+A Senior Vice President, and University of Dayton’s...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This is the second article in a three-part thought leadership...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

An email from your CRM vendor states that it suffered...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This is the first article in a three-part thought leadership...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Kate Azizi, Vice President for Institutional Advancement at the Medical...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In the webinar, "Fundraising campaigns in the time of COVID-19,"...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In August, more advancement offices have reopened for in-person work...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The COVID-19 pandemic has left the fundraising world reeling. As...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

At roughly the same time that the pandemic forced much...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Engaging our constituents has always been at the heart of...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

John Glier, GG+A CEO, and Mark Luellen, Vice President for...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In week 17 of the SurveyLab tracking of fundraiser outlook,...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

COVID-19 and its economic aftermath have caused a brute reckoning,...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In this webinar, GG+A’s Dan Lowman and Adrian Salmon walk...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In this week’s SurveyLab tracking of fundraiser outlook, participants demonstrated...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Carnegie Mellon’s take on Giving Tuesday, #givingCMUday, has been an...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The COVID-19 pandemic forced advancement teams to pivot abruptly to...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Mexico’s largest private, nonprofit university system, which encompasses 25 campuses...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Prior to the COVID-19 pandemic, most higher education institutions recognized...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

You did the impossible. Overnight, you pivoted from donor events,...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In normal times, fundraising follows a consistent path. While the...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Like many universities, Rice University has focused on its commitment...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This post was updated on Aug. 17. In this webinar,...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The 30-day high impact to fundraising jumped this week to...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

When you look in the mirror in the morning, do...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Early this spring, seemingly overnight, the time-tested habits of Advancement...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Fundraising outlook overall continues to improve, while crowdsourcing and giving...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

When a recent mini campaign planning study at Harvard T.H....

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The internet’s ability to maintain connections has been crucial to...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Negative fundraising outlooks for the next 30, 60 and 90...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

New Zealand is ahead of the pandemic curve compared to...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

GG+A's Independent Schools practice recently hosted a webinar highlighting how...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Fundraiser outlook over the next three months is holding steady,...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Editor's note: This statement was issued on behalf of GG+A...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Earlier this week, GG+A’s leadership put out a statement addressing...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The 30-, 60-, and 90-day fundraising outlooks have found a...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In the webinar, "Stewardship During the COVID-19 Pandemic and Beyond,”...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The fundraising outlook for the next 30, 60, and 90...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In November 2011, I was finishing my 15th year as...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

I’ll start by saying: look, I get it. We’ve all...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In the webinar, "Redefining How We Engage with the University’s...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In this webinar, GG+A Vice Presidents Adrian Salmon and Jason Shough...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

For the first time since tracking began, fundraising outlooks for...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In this webinar, Jeff Nearhoof, GG+A Senior Vice President, talks...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

GG+A's latest webinar features GG+A Senior Vice Presidents Melinda Church...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Editor's note: This article was updated on July 7 There’s...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Most nonprofit organizations know the benefits of performing a wealth...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Fundraising offices continue to be increasingly positive in their outlook...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

How are nonprofits—from local arts organizations to major research universities—staying...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Last month, GG+A hosted the webinar, “How Arts and Cultural...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Throughout the current crisis, GG+A's team has been responding to...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In college, I was fortunate enough to spend a semester...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The social and economic issues brought on by the pandemic...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

While your zoo, aquarium, museum or cultural institution may be...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Fundraisers were slightly more optimistic this week than last, according...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Editor's note: This article was updated on May 29 We’ve...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In this webinar, GG+A CEO John Glier talks to Anthony...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

On April 17, GG+A hosted a webinar with guest Marc...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In this webinar, GG+A CEO John Glier talks to Cindy...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Most organizations think of data governance as just another thing...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Robert J. Spiller, Assistant Secretary for Advancement for the Smithsonian...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In this webinar, "Impact of COVID-19 on Higher Education: Immediate...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The outlook for fundraising is turning more negative after four...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This unprecedented health and economic crisis that we are all...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Editor's note: This post was updated on June 11, 2020....

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In this webinar, Marc Weinstein, Vice-Principal of University Advancement at...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Sentiment for the next 30 and 60 days out continues...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

It’s challenging to navigate the philanthropic landscape amid a global...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Editor's note: This is Part II of a two-part response...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Editor's note: This is Part I of a two-part response...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Crises strike every organization. Data systems are breached. Research protocols...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In late February, the NorthShore University HealthSystem Foundation team was...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Fundraiser sentiment has been steadily improving since the beginning of...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Since my last blog post, my GG+A colleagues and I...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

As our academic medical centers, health care systems, and community...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Independent schools face unique challenges, and this remains true during...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

GG+A Vice President Adrian Salmon recently conducted a webinar on...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Nonprofit organizations are becoming increasingly comfortable with remote activity and...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

GG+A’s latest webinar, “Fundraising for the Nation’s Museums: Planning and...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

One of the more recent casualties of COVID-19 in the...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Most of us have seen the recent reminders on social...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Small development shops know how important and transformational planned gifts...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Most nonprofit organizations have moved to a fully remote development...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

GG+A's latest webinar, “Making Relationships Matter: UCLA Advancement Program’s Response...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In the wake of the COVID-19 crisis, the team at...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Unsurprisingly, there are high levels of concern and uncertainty across...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

I’ve spent the past week reaching out to my annual...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

As nonprofits scramble to navigate the current crisis, the team...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

COVID-19-related news is producing tremendous uncertainty. There’s so much information...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

(Editor's note: This article originally appeared in the Chronicle of...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Five principles to guide advancement professionals as you reach out...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

One day. 4,995 donors. $1,164,487 raised to fund programs, teams,...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

University of Pennsylvania Law School will lead students and alumni...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Employees who have no chance to utilize newfound knowledge forget...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

GG+A has partnered with institutions around the globe helping them...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Grenzebach, Glier and Associates CEO John Glier joins a distinguished...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

On June 9, 2019, hundreds of thousands of Hong Kong...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The American Association of Art Museum Curators recently released their...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Nonprofit Research Collaborative has released their Winter 2019 survey report. ...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The new Schwartz Reisman Innovation Centre will turbocharge the next...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This article is the seventh and final installment in a...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In addition to the many valuable new features in DonorScape...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This article is the sixth installment in a series. Read...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This article is the fifth installment in a series. Read...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This article is the fourth in a series. Read more...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Mary K. Carrasco, Assistant Head of School for Advancement at...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

DonorScape quickly identifies top donor prospects for efficient fundraising, but...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This article is the third installment in a series. The...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This article is the second installment in a series on...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

What organizations help you connect with fellow fundraising professionals in...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This is the time of year when many people think...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Donors overwhelmingly report that they are not seeing the impact...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

“Hong Kong overtook New York to become the world’s largest...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Hi, my name is Casey. I’m the new business development...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In 2016, President Tim Sands of Virginia Tech set a...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The University of Calgary (UCalgary) launched Energize: The Campaign for...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

GG+A’s Survey Lab has developed a Donor Experience Scorecard that...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The future is female, or at least the future of...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Nancy Gillece leads Hood College’s Office of Institutional Advancement, which...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

It is no secret that social media is becoming an...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The Segerstrom Center for the Arts “believes in the power...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Women’s boards represent a unique fundraising institution with a long,...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Giving USA noted that in 2017, corporate giving grew at...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Nestled in the Blue Ridge Mountains of northwestern North Carolina,...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

For a long time, the word “alumni” referred only to...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

A new survey of 231 college administrators conducted by the...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

If you had a chance to tune into GG+A’s recent...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Donor segmentation is not a new concept for most nonprofit...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The Giving Institute and Giving USA Foundation recently brought together...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Connecting to the ever-growing millennial donor population has been a...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In 2005, Thomas L. Friedman told us "The World is...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

As I watched a recent CBS 60 Minutes segment, I...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

By Rachel Schwimmer In a time of unpredictable government economic...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The rally cry for data was loud and clear at...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

By Rachel Schwimmer - A recent GG+A Survey Lab study...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Respondents are very philanthropic and plan to be so in...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

At some point in our careers, it is inevitable that...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

By Rachel Schwimmer According to a new study by GG+A...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

By Rachel Schwimmer A new GG+A Survey Lab study finds...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

By Felipe Hernandez A new GG+A Survey Lab study finds...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

A new study by the GG+A Survey Lab finds that...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Strong, effective stewardship programs are a core element of fundraising...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

If you work with prospects in their late 60s or...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

It was the memo heard around the world. In December...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Most fundraisers and their managers very appropriately have their eye...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Earlier this year, the Council to the Aid of Education...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

A few months ago, an independent school client asked us...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Purdue University: A case study in sustaining fundraising success through...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Imagine that you’re a development director and manager for a...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

A client recently wanted to produce a data visualization that...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

“You know I love the school, but I just can’t...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The number of financially independent, separately incorporated alumni associations has...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

“Does it sing and dance?” With a piercing glance, my...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

This article is based on a presentation developed for Building...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

International fundraising can complement an organization’s traditional efforts and greatly...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

“It is a far, far better thing that I do,...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In December 2016, the Information Commissioner (UK) fined the RSPCA...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

I am privileged to work with a diverse array of...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Animals can’t raise money to help protect their habitats, improve...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Predictive analytics streamlines and complements prospect research. Yet it can...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In decades of working with premier fundraising organisations worldwide and...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Thank you to all who could join GG+A last night...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In the first two blog posts of GG+A’s Ross-CASE Survey...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In our previous Ross-CASE blog, my colleague Adrian Salmon...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Recently my GG+A colleagues and I presented our analysis of...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Supplemental data is available for just about anything you might...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Some years ago when I was an experienced gift officer...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

With enormous time commitments, a wide variety of duties, and...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

I once had a conversation with a prospective donor who...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

After three years of anticipation, the San Francisco Museum of...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The list of skills gift officers must possess is a...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

A few days ago, Shakespeare fans around the world united...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

GG+A Vice President Adrian Salmon will present a day-long workshop...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The independent school sector has a multitude of opportunities to...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

CASE social media leaders and practitioners who gather this week...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Prospect Wealth Ratings can be tremendously valuable in setting the...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

According to a 2015 study by the National Endowment for...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

My GG+A colleagues in the US have been taken aback...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Andrew Gossen, Senior Director for Social Media Strategy, Alumni...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

By Ken Ashworth, Former Senior Vice President, Training and...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Last week I attended the CASE-NAIS annual conference in New...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

By Suzanne Hilser-Wiles Planning for the CASE NAIS conference this...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Is it possible to prove the value of alumni relations?...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Regular giving is now most definitely multi-channel. The mean number...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Defining alumni relations can help us articulate our purpose--and help...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

One of the most common reasons our clients ask for benchmarking...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

In partnering with their development colleagues in fundraising initiatives involving...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Recently, the notion of international markets as a growth opportunity has taken hold...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

"The new regulations have been tightened as a result of...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

“Our challenge is to build a prospect pool that is...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

You're the type who never gives up. But sometimes, letting...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Studies show that people around the world are naturally inclined...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

A data collection technique that forces respondents to choose a...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The Giving USA 2015 Report on Philanthropic Giving, the annual report on...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The Giving USA 2015 Report on Philanthropic Giving, the annual report on...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The Giving USA 2015 Report on Philanthropic Giving, the annual report on...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The Giving USA 2015 Report on Philanthropic Giving, the annual report on...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The more I peruse the literature on women’s philanthropy, the more...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

First you gotta crawl, then walk… and then you can...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

How can a small development team with a big fundraising...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

As news is created and distributed at a previously unimaginable...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

So many museums suffer what some might consider a “happy...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

The term “big data” may be the buzz word of...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

Effective case statements consist of compelling prose that, while appealing...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png

I am a sports fan (or fanatic, some might say);...

Grenzebach Glier & Associates Inc

http://gga.ugmade.co/wp-content/themes/gga/assets/img/grenzebach-glier-and-associates-print-only.png